Digital Newsletter

Each week our editor Phil Alsop rounds up the most popular articles, videos and expert opinions. We compile this into a Digital Newsletter and send it straight to your inbox every week.

Digital Magazines

We'll let you know each time a new edition of Digitalisation World is released so that you're always kept up-to-date with the latest and greatest news and press releases.

Video Magazines

The Digitalisation World Video magazine contains the latest Zoom interviews with experts in the industry.

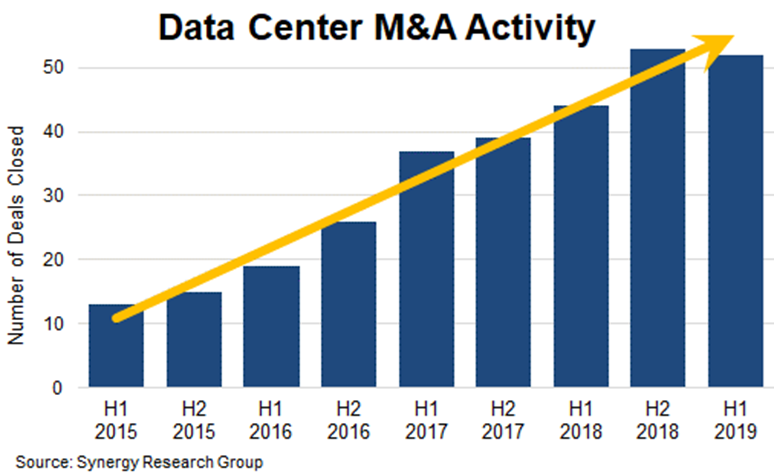

In terms of deal value the story is a little different from deal count as the trend is skewed by a very small volume of huge multi-billion dollar acquisitions. Eleven such deals were closed during the 2017-2018 period, while 2019 has yet to see a multi-billion deal closure. Since 2015 the largest deals to be closed are the acquisition of DuPont Fabros by Digital Realty, the Equinix acquisition of Verizon’s data centers and the Equinix acquisition of Telecity. Over the 2015-2019 period, by far the largest investors have been Equinix and Digital Realty, the world’s two leading colocation providers. In aggregate they account for 36% of total deal value over the period. Other notable data center operators who have been serial acquirers include CyrusOne, Iron Mountain, Digital Bridge/DataBank, NTT and Carter Validus.

“Analysis of data center M&A activity helps to affirm some clear trends in the industry, not least of which is that enterprises increasingly do not want to own or operate their own data centers,” said John Dinsdale, a Chief Analyst at Synergy Research Group. “As enterprises either shift workloads to cloud providers or use colocation facilities to house their IT infrastructure, more and more data centers are being put up for sale. This in turn is driving change in the colocation market, with industry giants on a never-ending quest to grow their global footprint and a constant ebb and flow of ownership among small local players. We expect to see a lot more data center M&A over the next five years.”